Comment

What are the implications of the June 2026 Minimum Energy Efficiency Standards interim response?

The Government has now confirmed the direction of travel for Minimum Energy Efficiency Standards (MEES) in the non-domestic private rented sector in England and Wales. Below we outline what has been announced, why and the potential implications.

The Government update is an interim response to earlier consultations and the headline is a more targeted approach than previously proposed: EPC B is still in view, but only for larger rented buildings over 1,000 sq m, with the interim EPC C milestone dropped.

That shift matters. It changes the likely compliance burden across the market, gives more time for upgrades, and creates a clearer distinction between larger commercial assets and smaller premises. For landlords, investors, developers and occupiers, this is less a retreat from energy performance regulation than a recalibration of where Government believes intervention will have the biggest impact.

What has been announced?

In its interim response on non-domestic MEES, the Government has confirmed its intention to implement the following [1]:

- From 2031, private rented non-domestic buildings over 1,000 sq m would need to achieve EPC B, where cost effective.

- Buildings below 1,000 sq m would continue to be subject to the current EPC E minimum standard.

- The previously proposed interim EPC C milestone for 2027 will not be taken forward.

- Existing flexibility mechanisms, including the 7-year payback test and current exemptions, are intended to remain in place.

These changes will only take effect once the necessary secondary legislation has passed through Parliament, with further detail to come in a fuller Government response and updated guidance.

Why has Government taken this approach?

The interim response frames the policy around proportionality, affordability and impact. Government says the targeted approach is designed to support businesses occupying larger premises, reduce energy costs, strengthen energy security and cut carbon emissions, while avoiding an unduly heavy burden on smaller landlords and tenants. It also states that tenants in the largest rented buildings could save £360 million per year by 2031, although that figure is described as subject to refinement.

The message is therefore twofold:

- Energy efficiency regulation is still advancing, especially for larger stock.

- Government is trying to match ambition with deliverability, particularly in a market facing cost, viability and leasing constraints.

What does this mean for landlords?

For landlords with larger non-domestic rented assets, the direction of travel is now clearer. EPC B remains the likely target, with 2031 providing a little more leeway than expected. However, improvement works on larger commercial buildings can be technically complex, capital intensive and dependent on occupation patterns, MEP upgrades, facade constraints and lease structure.

For landlords of smaller assets below 1,000 sq m, the immediate pressure is lighter. But that does not remove the commercial importance of energy performance. Even where regulation remains at EPC E; market expectations, tenant demand, financing conditions and corporate ESG objectives may still pull assets toward higher standards.

What does this mean for occupiers?

Occupiers, particularly those in larger buildings, should expect MEES to become more relevant in lease negotiations, dilapidations strategies, service charge planning and wider workplace decisions. If a building will need to move toward EPC B, that can influence the timing and scope of landlord works, the viability of lease renewals, and the allocation of upgrade costs.

Buildings that perform better are often better placed to offer occupiers lower running costs, improved resilience and stronger long-term leasing prospects. Even where legal compliance is some years away, the commercial conversation is already here.

The continuing importance of exemptions and cost effectiveness

One of the more important elements of the announcement is what has not changed. The Government intends to keep the existing 7-year payback test and current exemptions, underlining that the policy should only require improvements that are practical, affordable and cost effective.

However, here a fundamental methodological flaw of EPCs must be recognised in that they rely on theoretical models rather than actual operational data. There has been a gradual shift in the market with Energy Use Intensity (EUIs) recognised as the new metric for benchmarking and net zero assessments, popularised by the Carbon Risk Real Estate Monitor (CRREM) and more recently, the UK Net Zero Carbon Buildings Standard (UKNZCBS).

Therefore, targeting low-cost interventions that materially improve both EPC performance and operational energy consumption will be the litmus test for successful MEES compliance strategies.

Sectoral implications industrial and retail

Over 90% of industrial and retail properties in England and Wales have an EPC E or above. However, this percentage drops significantly for those with an EPC of B or above. Around 40% of supermarkets and retail parks meet this coming requirement, but only 14% of shopping centres and 10% of industrial buildings do so [2].

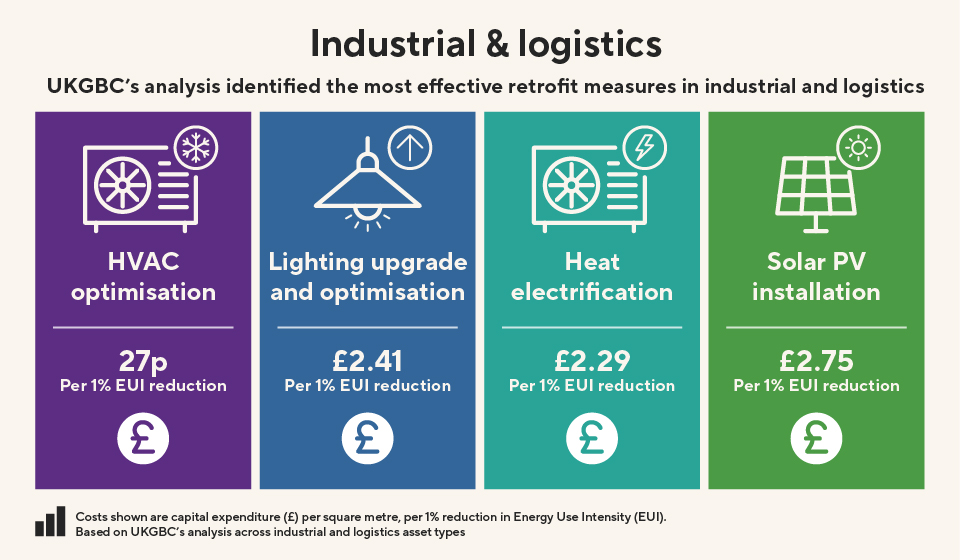

Industrial and logistics

The industrial and logistics sector is generally better positioned to respond to higher MEES requirements. Large roof areas suitable for solar PV, relatively simple building services and lower occupancy densities often make energy performance improvements more straightforward than in complex office environments. UKGBC's guidance for a logistics warehouse identifies HVAC optimisation (27p / 1% EUI reduction), Heat Electrification (£2.29/ 1% EUI reduction), Lighting Upgrade and Optimisation (£2.41 / 1% EUI reduction) and Solar PV Installation (£2.75 /1% EUI reduction) as the most cost-effective measures [2].

However, older industrial stock and manufacturing facilities may still face challenges where building fabric, heating systems or specialist operational requirements limit available improvement measures.

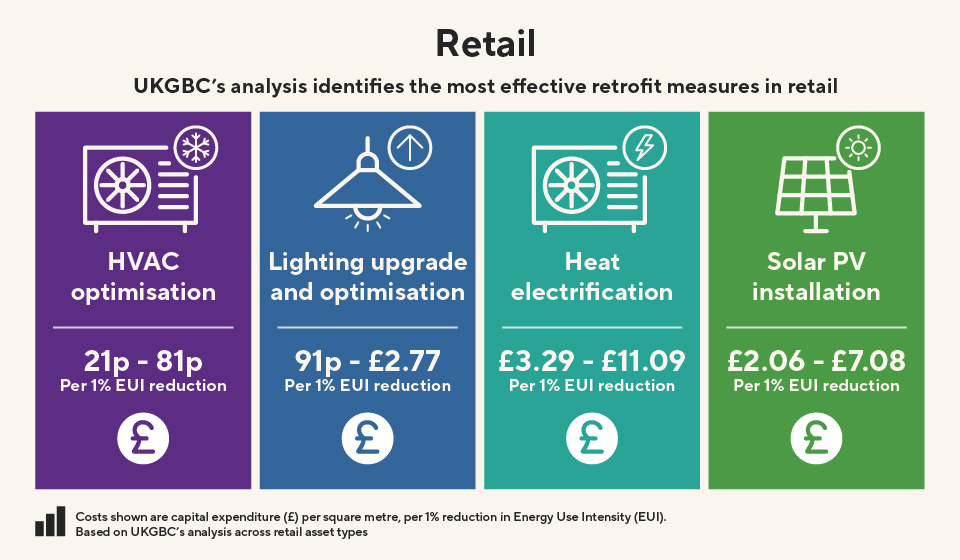

Retail

The retail sector faces a more complex pathway to meeting higher MEES requirements than industrial and logistics assets. Retail buildings typically have longer operating hours, higher occupant densities, larger conditioned sales areas and more intensive HVAC demands, while supermarkets also have significant refrigeration loads. These characteristics make energy performance improvements more challenging and increase the importance of operational optimisation.

UKGBC's analysis identifies HVAC optimisation (21p - £0.81 per 1% EUI reduction), lighting upgrades and optimisation (91p - £2.77 per 1% EUI reduction), heat electrification (approximately £3.29 - £11.09 per 1% EUI reduction) and solar PV installation (approximately £2.06 - £7.08 per 1% EUI reduction) as the most cost-effective measures across retail asset types [2]. HVAC optimisation was the most cost-effective intervention for traditional high street retail, retail warehouses and supermarkets, while lighting upgrades were particularly effective in restaurant environments. Heat electrification delivered some of the largest energy reductions, typically reducing Energy Use Intensity (EUI) by around 23-24%, while solar PV offered particularly strong benefits for retail warehouse formats with large roof areas. However, older high street retail assets, shopping centres and supermarkets may face greater challenges where ageing building fabric, extensive glazing, landlord-tenant split incentives, refrigeration systems and constrained plant space limit the range and affordability of retrofit interventions. Regular optimisation, targeted lighting upgrades and planned electrification of heating systems are therefore likely to form the foundation of cost-effective retail decarbonisation strategies.

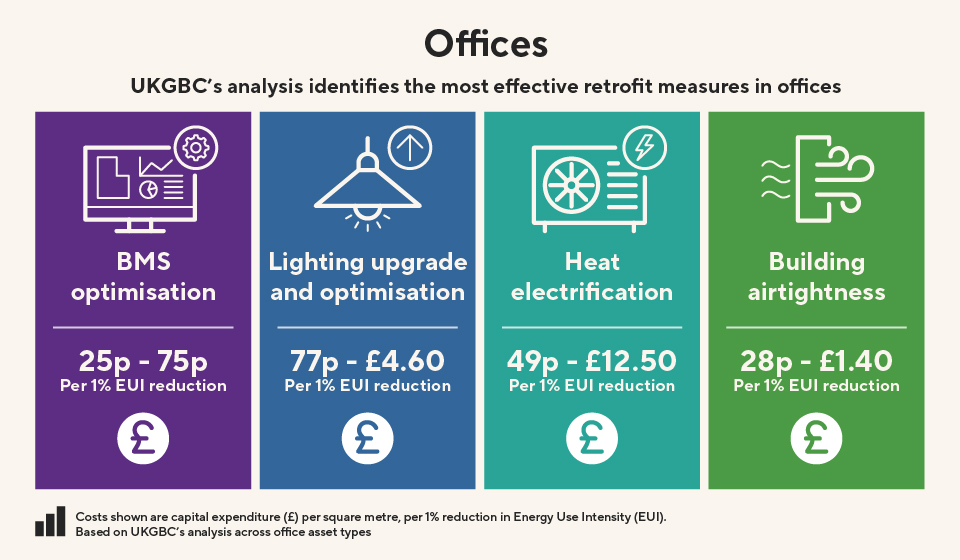

Sectoral implications – offices

Analysis of EPC data quoted by UKGBC indicated that 77% of UK office stock is currently rated below EPC B[3]. The office sector faces a distinctive pathway to meeting higher MEES requirements, balancing increasingly stringent energy performance expectations with evolving occupier demands, hybrid working patterns and the need to avoid asset obsolescence. Office buildings are complex, dynamic systems where energy consumption is influenced not only by building fabric and services, but also by occupant behaviour, tenancy arrangements and operational practices. As a result, optimisation measures often deliver a greater proportion of energy savings than in other commercial sectors.

UKGBC's analysis [3] identifies building management system (BMS) optimisation and tenant load reduction as the most cost-effective interventions, capable of reducing Energy Use Intensity (EUI) by around 27% at very low cost; but linked to none or negligible EPC improvements. At the other end, the decarbonisation of heat reduces EUI by 18% and has a high EPC impact. Beyond optimisation, light retrofit measures can collectively reduce office EUI by approximately 15%, whilst deep retrofit programmes incorporating fabric upgrades, heat electrification and ventilation improvements can achieve total EUI reductions of 66%, bringing many assets close to emerging net zero energy performance targets.

Summary

The Government's announcement may have eased the immediate compliance burden for many landlords, but it has not altered the long-term direction of travel. Energy performance is becoming an increasingly important determinant of asset value, occupier demand, financing conditions and investment risk. The organisations that will benefit most from this shift will be those that use the time to identify cost-effective interventions, align retrofit investment with wider asset strategies and improve both EPC performance and real-world energy consumption.

If you would like to continue the conversation on how the proposed changes could affect your portfolio please contact Director, Head of ESG, Snigdha Jain.

26 June 2026

[1] Minimum Energy Efficiency Standards (MEES) in the non‑domestic Private Rented Sector: interim response

[2] https://ukgbc.org/resources/building-the-case-for-net-zero-retrofitting-retail-and-logistics-buildings/

[3] https://ukgbc.org/resources/building-the-case-for-net-zero-retrofitting-office-buildings/

The data in the infographics included in this article has been taken from UKGBC research:

You may also be interested in

News

12 February 2026

Planning consent secured for the transformation of London Stock Exchange Group headquarters

Turley provided expert Heritage & Townscape and Sustainability & ESG services to Oxford Properties Group (“Oxford”), the global real estate investor, ...

News

1 October 2025

Planning secured to retrofit Santander’s former HQ, 201 Grafton Gate in Milton Keynes

On behalf of Osborne+Co, Turley has secured planning approval for the comprehensive refurbishment and extension of 201 Grafton Gate, the former ...

Project

London Stock Exchange Group (LSEG), City of London

| Client | Oxford Properties Group |

|---|---|

| Turley office | London |

| Status | Planning permission granted |